$JDEP Quick Pitch

JDE Peet's N.V. is an American-Dutch multinational coffee and tea company headquartered in Amsterdam

$JDEP #QuickPitch mcap= €8.00B, price €16.38 / share

$JDEP #Pitch:

JDE Peet’s N.V. is a global leader in coffee and tea, owning brands such as Jacobs, L’OR, Peet’s, and Senseo. The company operates in both in-home and far-away coffee markets and has a strong presence in premium and specialty coffee categories.

The company holds top #1 or #2 rankings in 39 markets, offering a wide array of products through over 50 global, regional, and local brands. JDE Peet’s employs a vertically integrated business model, overseeing the entire process from sourcing coffee beans to distributing to final consumers.

Focused on premiumization, brand extensions, and strategic partnerships, JDE Peet’s continues to expand its market presence and product offerings. The company maintains local autonomy and accountability, allowing regional leadership to drive tailored market strategies while benefiting from a global scale.

In October 2024, JAB, the majority shareholder of JDE Peet’s, increased its stake to 68% by acquiring Mondelez’s 17.6% share for €2.2 billion, €25.10 / share. This transaction also increased the free float to 32%, enhancing the company's market liquidity.

Rafael Oliveira, a former executive at Kraft Heinz, was appointed as the new CEO, effective November 1, 2024, bringing fresh leadership to drive the company's strategic initiatives. The management has emphasized the need for a better balance between short-term profitability and long-term investments, particularly in R&D and marketing.

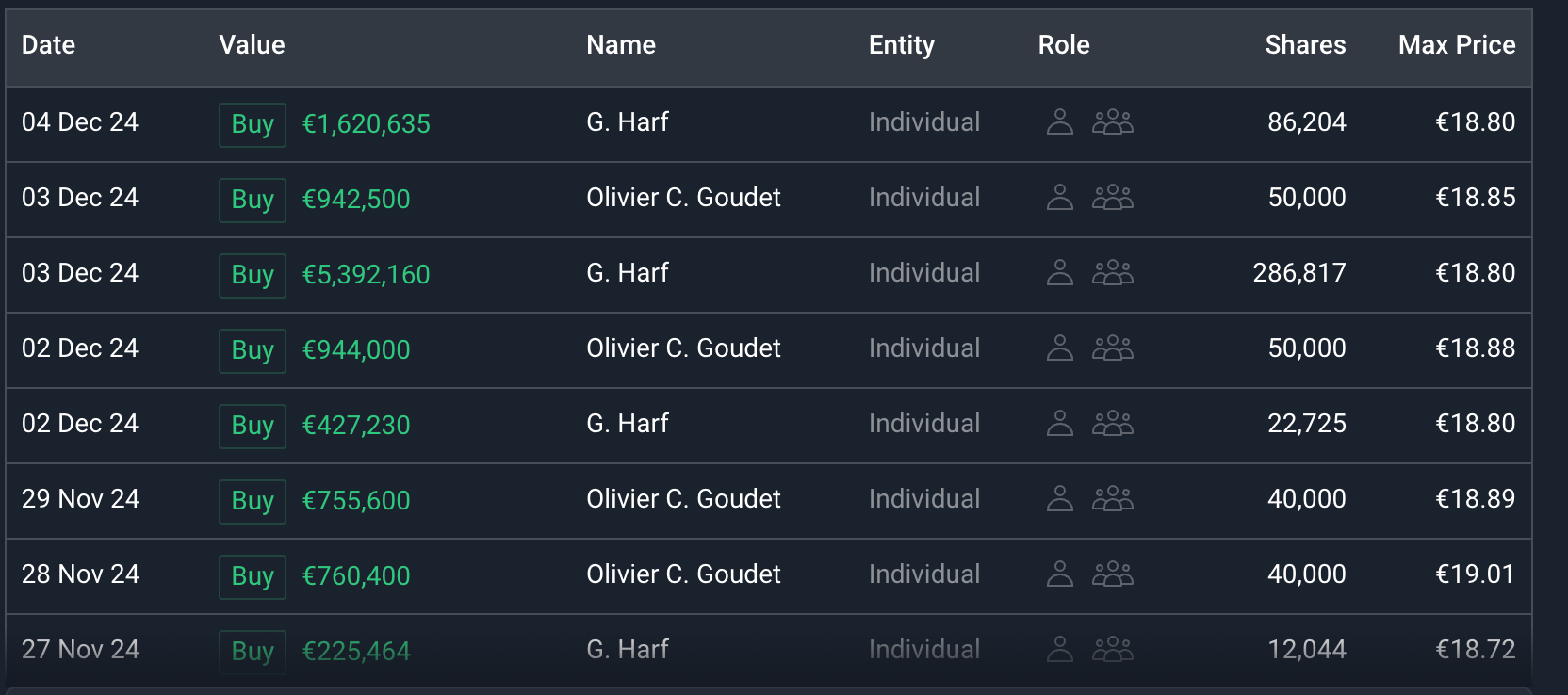

Recent insider transactions reveals that management belives in the long term potential of the business, buying in lots of shares for around €18 / share.

The company has continued to expand its premium and specialty offerings, launching Peet’s premium coffee expansion in the U.S., L’OR Barista Passiona Rossa espresso range, and Pickwick Superblends extension, catering to the growing demand for premium teas.

Green coffee price inflation continues to be challenging, requiring disciplined cost management. Arabica coffee prices are especially impacted, as Brazil, the crop's largest producer, faced a lengthy drought in 2024, leading to poor crop estimates for the upcoming year. Because of this, as International Comunicaffe reported, Volcafe specialists cut their 2025 and 2026 forecast for Arabicas to 34.4 million bags, down nearly 11 million bags from the September estimate.

Pricing issues were also compounded this week by President Donald Trump's threat to enact a 25% tariff on Colombian goods if the country did not allow his deportation planes to land in the nation.

Inflationary cost pressures on green coffee prices remain a risk, though JDE Peet’s has effectively navigated rising costs through strategic pricing and cost management.

The successful integration of Maratá and Caribou Coffee (acquired in early 2024) has been on track with expectations. JDE Peet’s has aligned away-from-home (AFH) and consumer-packaged goods (CPG) strategies, optimizing its market reach and operational efficiencies.

$JDEP #Valuation:

Organic sales growth was +3.6%, supported by a 5-year CAGR of +5.0%. The growth was broad-based across geographies and product categories, with premium product offerings driving higher margins.

Europe delivered +14.1% EBIT growth, driven by cost management and margin expansion. APAC & Peet’s US EBIT growth of 60.1% and 41.7%, reflects strong consumer demand and premium product expansion.

Net leverage increased to 3.12x, reflecting the impact of recent acquisitions. However, the company continues to generate strong free cash flow (€315M in H1 2024), supporting debt reduction and shareholder returns.

JDE Peet’s has a well-structured debt maturity profile, ensuring manageable repayment obligations in the coming years. The company maintains strong free cash flow (€315 million in H1 2024), which supports ongoing deleveraging efforts and interest payments. Net Debt: €4.78 billion, up from €3.89 billion due to the Maratá and Caribou acquisitions.

The average Debt Maturity is 4.2 years, providing stability in refinancing with an average Cost of Debt of 1.1%, indicating a low-interest burden compared to industry peers.

As long as the leverage reduction remains a priority, with a focus on bringing net debt below 3x EBITDA, I see no short-term liquidity concerns, as future maturities are well below free cash flow levels.

Expected Gain: JDEP seems to be a compelling opportunity at the current price, for a 10-12% return dividend included. In my opinion, I see the cash flow of this company between €650m to €1B so the company should be at least €22 / share.